“`html

The acid-test ratio, also known as the quick ratio, is a liquidity ratio that measures a company’s ability to meet its short-term obligations using its most liquid assets. It’s a more stringent measure than the current ratio because it excludes inventory from the calculation. Inventory, while technically a current asset, can be difficult to convert quickly into cash, potentially skewing the true picture of a company’s immediate solvency. In situations where inventory turnover is slow or difficult, the acid-test ratio offers a more realistic assessment.

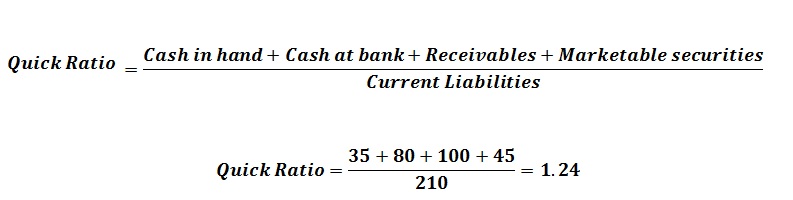

The formula for the acid-test ratio is: (Cash + Marketable Securities + Accounts Receivable) / Current Liabilities. Let’s break down each component:

- Cash: This includes readily available cash on hand and in bank accounts.

- Marketable Securities: These are short-term investments that can be easily converted into cash, such as treasury bills or commercial paper.

- Accounts Receivable: This represents money owed to the company by its customers for goods or services already delivered.

- Current Liabilities: These are obligations due within one year, such as accounts payable, salaries payable, and short-term debt.

The higher the acid-test ratio, the better positioned a company is to cover its immediate liabilities. A ratio of 1 or higher generally indicates that a company has sufficient liquid assets to cover its current debts. A ratio below 1 suggests that the company might struggle to meet its short-term obligations using only its most liquid assets. However, the ideal acid-test ratio can vary depending on the industry. Some industries, like software, may have lower inventory needs and thus can operate successfully with a lower ratio. Conversely, industries with significant inventory, such as retail, may typically maintain a lower ratio and compensate through efficient inventory management.

It’s crucial to remember that the acid-test ratio is just one indicator of financial health. Relying solely on this metric can be misleading. For instance, a high acid-test ratio may also signal inefficient use of cash. A company might be holding too much cash instead of investing it for growth. Similarly, a low ratio doesn’t automatically spell disaster. A company might have secured lines of credit or well-established relationships with suppliers that allow it to manage short-term liabilities effectively. Therefore, the acid-test ratio should be analyzed in conjunction with other financial ratios and qualitative factors to gain a comprehensive understanding of a company’s financial position.

In conclusion, the acid-test ratio is a valuable tool for assessing a company’s immediate liquidity, providing a more conservative view than the current ratio. However, it’s essential to interpret the ratio within the context of the industry and the company’s specific circumstances, considering it alongside other financial metrics to form a complete picture of its financial health.

“`

1280×720 acid test ratio finance reference from www.financereference.com

1280×720 acid test ratio finance reference from www.financereference.com  474×406 acid test ratio meaning formula interpretation efm from efinancemanagement.com

474×406 acid test ratio meaning formula interpretation efm from efinancemanagement.com  903×403 acid test ratio learn calculate acid test ratio from corporatefinanceinstitute.com

903×403 acid test ratio learn calculate acid test ratio from corporatefinanceinstitute.com  768×384 acid test ratio shabbir bhimani from shabbir.in

768×384 acid test ratio shabbir bhimani from shabbir.in  350×263 liquidity ratios current ratio acid test ratio balance sheets from www.teacherspayteachers.com

350×263 liquidity ratios current ratio acid test ratio balance sheets from www.teacherspayteachers.com  472×301 easy guide acid test ratio from www.f9finance.com

472×301 easy guide acid test ratio from www.f9finance.com  474×266 acid test ratio formula calculator updated from wealthyeducation.com

474×266 acid test ratio formula calculator updated from wealthyeducation.com  700×700 acid test ratio fundsnet from fundsnetservices.com

700×700 acid test ratio fundsnet from fundsnetservices.com .jpg) 835×572 acid test ratio interpretation investinganswers from investinganswers.com

835×572 acid test ratio interpretation investinganswers from investinganswers.com  608×325 acid test quick accounting ratio calculation current from www.accountingscholar.com

608×325 acid test quick accounting ratio calculation current from www.accountingscholar.com  1830×1070 complete guide understanding acid test ratio from www.deskera.com

1830×1070 complete guide understanding acid test ratio from www.deskera.com  1000×667 acid test ratio financeeconomy folder desk label from stock.adobe.com

1000×667 acid test ratio financeeconomy folder desk label from stock.adobe.com  1024×461 acid test ratio meaning formula calculation examples from www.wallstreetmojo.com

1024×461 acid test ratio meaning formula calculation examples from www.wallstreetmojo.com  600×315 acid test ratio accountingcapital from www.accountingcapital.com

600×315 acid test ratio accountingcapital from www.accountingcapital.com  768×576 acid test ratio detailed explanation financial solvency analysis from inspiredeconomist.com

768×576 acid test ratio detailed explanation financial solvency analysis from inspiredeconomist.com  793×200 calculate acid test ratio from pediaa.com

793×200 calculate acid test ratio from pediaa.com  638×479 mastering acid test ratio accounting business liquidity from www.cgaa.org

638×479 mastering acid test ratio accounting business liquidity from www.cgaa.org  1280×720 acid ratio superfastcpa cpa review from www.superfastcpa.com

1280×720 acid ratio superfastcpa cpa review from www.superfastcpa.com  604×653 acid test ratio formula cailynaresvega from cailynaresvega.blogspot.com

604×653 acid test ratio formula cailynaresvega from cailynaresvega.blogspot.com  704×513 acid test ratio quick ratio formulaexampledefinition from www.projectcubicle.com

704×513 acid test ratio quick ratio formulaexampledefinition from www.projectcubicle.com  716×716 unlock liquidity potential acid test ratio quick ratio from finmodelslab.com

716×716 unlock liquidity potential acid test ratio quick ratio from finmodelslab.com  736×451 accounting acid test ratio formula jaimetewatkins from jaimetewatkins.blogspot.com

736×451 accounting acid test ratio formula jaimetewatkins from jaimetewatkins.blogspot.com  1200×1236 acid test ratio meaning formula examples from www.careerprinciples.com

1200×1236 acid test ratio meaning formula examples from www.careerprinciples.com  640×360 acid test ratio from www.moneybestpal.com

640×360 acid test ratio from www.moneybestpal.com  605×848 solved current ratio acid test ratio debtequity ratio cheggcom from www.chegg.com

605×848 solved current ratio acid test ratio debtequity ratio cheggcom from www.chegg.com  1200×640 answered financial ratios current ratio quick bartleby from www.bartleby.com

1200×640 answered financial ratios current ratio quick bartleby from www.bartleby.com  1086×588 accounting acid test ratio formula from giadesnhcrosby.blogspot.com

1086×588 accounting acid test ratio formula from giadesnhcrosby.blogspot.com