RD Finance’s Weighted Average Cost of Capital (WACC) is a crucial metric for evaluating the company’s overall cost of funding its operations and projects. WACC represents the average rate of return a company must earn on its existing assets to satisfy its investors (both debt and equity holders). In essence, it’s the minimum acceptable rate of return for any new investment that RD Finance undertakes.

The WACC formula is calculated as follows:

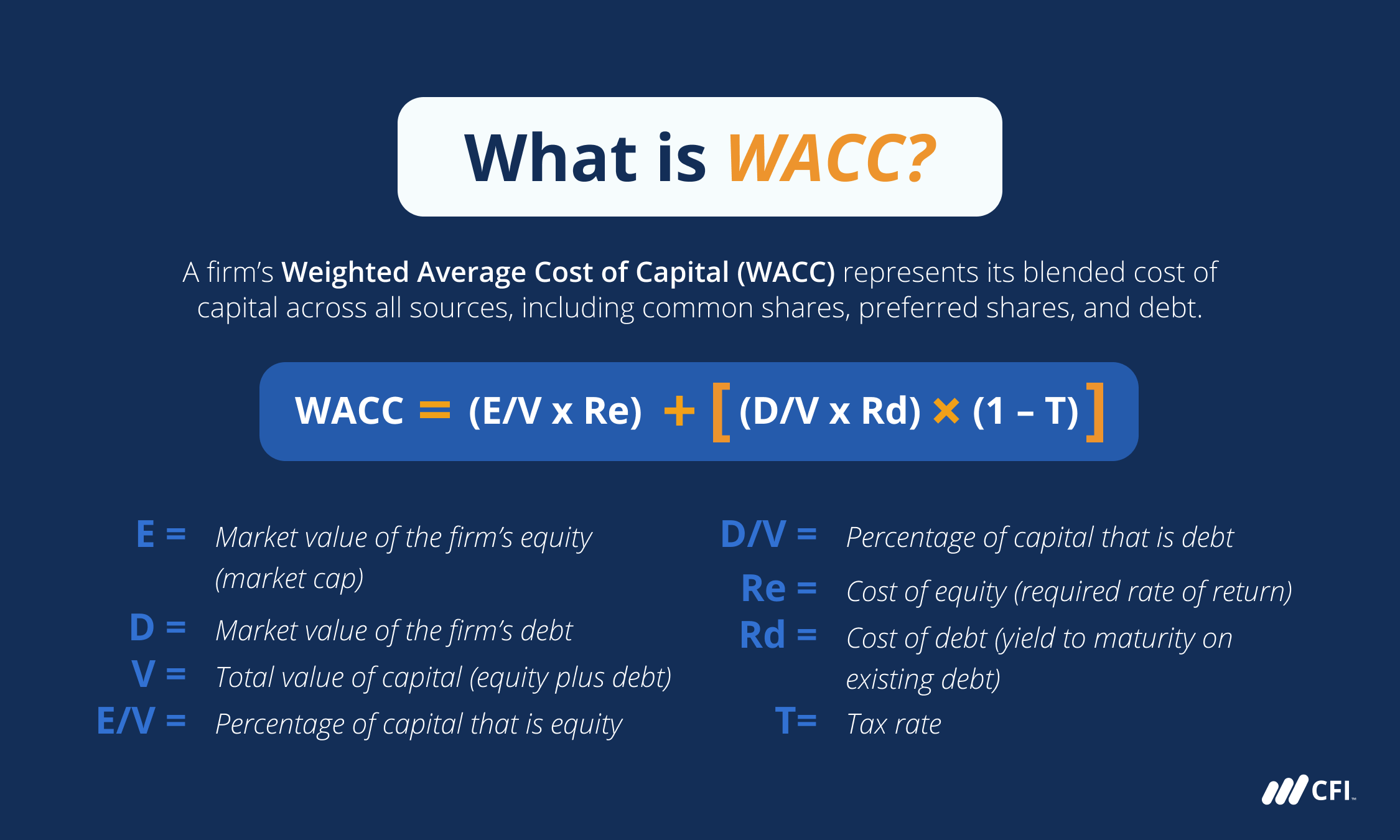

WACC = (E/V) * Ke + (D/V) * Kd * (1 – T)

Where:

- E = Market value of equity

- D = Market value of debt

- V = Total value of capital (E + D)

- Ke = Cost of equity

- Kd = Cost of debt

- T = Corporate tax rate

Let’s break down each component and how it applies to RD Finance:

Cost of Equity (Ke): Determining RD Finance’s cost of equity is often achieved using the Capital Asset Pricing Model (CAPM). CAPM considers the risk-free rate of return (e.g., yield on government bonds), the company’s beta (a measure of its volatility relative to the market), and the market risk premium (the expected return on the market above the risk-free rate). A higher beta implies greater risk and, consequently, a higher cost of equity for RD Finance.

Cost of Debt (Kd): RD Finance’s cost of debt is the effective interest rate the company pays on its debt. This is typically determined by analyzing the yield to maturity on RD Finance’s outstanding bonds or by assessing the interest rates on its loans. It’s important to consider the market value of debt, which might differ from the book value, especially if interest rates have fluctuated significantly.

Capital Structure (E/V and D/V): The proportions of equity and debt in RD Finance’s capital structure significantly impact the WACC. A higher proportion of debt, while potentially cheaper due to the tax shield (explained below), also increases financial risk. Conversely, a higher proportion of equity reduces financial risk but might be more expensive than debt. RD Finance’s management must carefully balance debt and equity to optimize its capital structure and minimize its WACC.

Tax Rate (T): The corporate tax rate plays a crucial role due to the tax deductibility of interest payments on debt. This tax shield effectively lowers the after-tax cost of debt, making debt a more attractive source of financing compared to equity. The term (1 – T) in the WACC formula reflects this reduction in the cost of debt. For RD Finance, understanding and accurately incorporating the applicable tax rate is essential.

A low WACC is desirable for RD Finance as it indicates that the company can attract capital at a lower cost, making its investment projects more profitable and increasing shareholder value. Changes in market interest rates, RD Finance’s credit rating, or its capital structure can all affect the company’s WACC. Therefore, regularly monitoring and analyzing WACC is vital for effective financial management and strategic decision-making at RD Finance.

780×482 wacc debt increases financestu from financestu.com

780×482 wacc debt increases financestu from financestu.com  803×318 calculating wacc formula examples calculator from www.educba.com

803×318 calculating wacc formula examples calculator from www.educba.com  512×512 wacc finance exploring basics benefits weighted from www.tffn.net

512×512 wacc finance exploring basics benefits weighted from www.tffn.net  335×292 relevering beta wacc financetrainingcoursecom from financetrainingcourse.com

335×292 relevering beta wacc financetrainingcoursecom from financetrainingcourse.com  585×360 weighted average cost capital wacc from www.daytrading.com

585×360 weighted average cost capital wacc from www.daytrading.com  2250×1350 wacc formula definition guide cost capital from corporatefinanceinstitute.com

2250×1350 wacc formula definition guide cost capital from corporatefinanceinstitute.com  1024×576 weighted average cost capital wacc formula examples from brunofuga.adv.br

1024×576 weighted average cost capital wacc formula examples from brunofuga.adv.br  1024×800 finance funding lending compare lenders from www.bulletpoint.com.au

1024×800 finance funding lending compare lenders from www.bulletpoint.com.au  1024×171 weighted average cost capital wacc forage from www.theforage.com

1024×171 weighted average cost capital wacc forage from www.theforage.com  180×233 wacc figurepptx elements wacc rs wacc from www.coursehero.com

180×233 wacc figurepptx elements wacc rs wacc from www.coursehero.com  625×100 weighted average cost capital wacc formula definition from www.myaccountingcourse.com

625×100 weighted average cost capital wacc formula definition from www.myaccountingcourse.com  716×325 roic wacc from joapen.com

716×325 roic wacc from joapen.com  640×512 solved wacc cheggcom from www.chegg.com

640×512 solved wacc cheggcom from www.chegg.com  1419×829 wacc wacc appreciated raccounting from www.reddit.com

1419×829 wacc wacc appreciated raccounting from www.reddit.com  1500×600 wacc roic highlights shareholder created destroyed from einvestingforbeginners.com

1500×600 wacc roic highlights shareholder created destroyed from einvestingforbeginners.com  903×708 wacc adjustment correct valuation tax shields edward bodmer from edbodmer.com

903×708 wacc adjustment correct valuation tax shields edward bodmer from edbodmer.com  350×144 wacc valuation business valuation specialists singapore from businessvaluation.com.sg

350×144 wacc valuation business valuation specialists singapore from businessvaluation.com.sg  980×516 wacc roic ultimate investment showdown stock analysis from www.theglobetrottinginvestor.com

980×516 wacc roic ultimate investment showdown stock analysis from www.theglobetrottinginvestor.com  800×800 relationship irr wacc wara valuology medium from valuology.medium.com

800×800 relationship irr wacc wara valuology medium from valuology.medium.com  1024×576 wacc quantify debt risk real estate investments from origininvestments.com

1024×576 wacc quantify debt risk real estate investments from origininvestments.com  1024×616 understanding weighted average cost capital wacc magnimetrics from magnimetrics.com

1024×616 understanding weighted average cost capital wacc magnimetrics from magnimetrics.com  804×1429 solved information presented exhibit cheggcom from www.chegg.com

804×1429 solved information presented exhibit cheggcom from www.chegg.com  1212×798 understanding weighted average cost capital wacc calculations daniel from danieel.id

1212×798 understanding weighted average cost capital wacc calculations daniel from danieel.id  583×383 wacc component part company specific risk premium from valuology.medium.com

583×383 wacc component part company specific risk premium from valuology.medium.com .png) 1280×720 deciphering debt risk private real estate investments role wacc from www.freedomventure.com

1280×720 deciphering debt risk private real estate investments role wacc from www.freedomventure.com